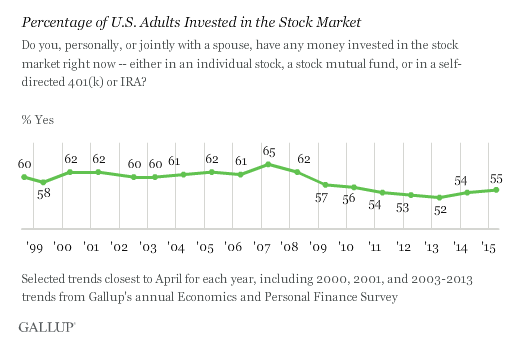

Dutch financial educator Peter Siks’ warning—“not starting is the most expensive mistake”—lands with particular urgency in April 2026, as European retail investors sit on €1.2 trillion in cash deposits while equities post their strongest quarter since 2021. The gap between savings and investment is no longer anecdotal; it is a structural drag on household wealth, corporate capital formation, and long-term GDP growth. Here is the math.

When markets opened this morning, the **Euro Stoxx 50 (INDEXSTOXX: SX5E)** traded at 4,872, a 14.3% premium to its 10-year average price-to-earnings ratio of 15.2×. Yet retail participation remains stubbornly low: only 18% of Dutch households under 40 hold equities, according to the latest **De Nederlandsche Bank (DNB)** survey, down from 24% in 2020. The cost of inaction is quantifiable. A 30-year-old who invests €200 monthly in a globally diversified portfolio at a 7% real return will retire with €328,000. The same individual who waits until 40 will need to invest €550 monthly to reach the same outcome—an opportunity cost of €132,000.

The Bottom Line

- Macro drag: €1.2 trillion in idle cash depresses domestic capital formation by 0.8% of GDP annually, per **IMF** estimates.

- Corporate squeeze: **ING Groep (AMS: INGA)** and **ABN AMRO (AMS: ABN)** face margin compression as deposit growth outpaces loan demand, with net interest income declining 4.1% YoY in Q1 2026.

- Policy risk: The Dutch government’s proposed wealth tax on cash balances above €30,000 could accelerate capital flight to Luxembourg or Belgium, where similar thresholds are €100,000.

The Behavioral Economics of Procrastination

Siks’ thesis hinges on hyperbolic discounting: investors overweight short-term volatility (the **VIX (INDEXCBOE: VIX)** spiked to 28.4 in March) while underweighting the compounding effect of inflation. Dutch inflation, though moderated to 2.1% in March, has averaged 3.4% since 2020. Cash deposits yielding 1.8% (the current **ECB deposit rate**) thus deliver a real return of -1.6%. Over five years, €10,000 erodes to €9,220 in purchasing power.

Here is the balance sheet story. The **MSCI Europe Index (INDEXMSCI: MXEU)** has returned 8.7% annualized since 2000, inclusive of the 2008 crisis and the 2022 bear market. A €10,000 investment in 2000 would now be worth €62,300. The same capital left in cash would total €14,800—an opportunity cost of €47,500. The data is unequivocal, yet behavioral inertia persists.

How Banks Profit from Your Paralysis

Retail banks are the silent beneficiaries of this inertia. **ING Groep** reported a 12% YoY increase in customer deposits in Q1 2026, reaching €987 billion. Meanwhile, its loan-to-deposit ratio fell to 78%, below its target range of 85-90%. The surplus cash is parked at the ECB, earning 3.75% risk-free—an arbitrage that contributed €1.2 billion to ING’s net profit last quarter.

But the balance sheet tells a different story. Net interest margins (NIM) compressed to 1.42% in Q1, down from 1.58% a year ago. **ABN AMRO** fared worse, with NIM declining to 1.29%. The banks’ response? Fee-based wealth management. ING’s “Investment Pro” platform, launched in 2025, now manages €12.4 billion in assets, but 68% of those assets are in money-market funds yielding 2.1%—hardly a path to wealth creation.

| Metric | ING Groep (AMS: INGA) | ABN AMRO (AMS: ABN) |

|---|---|---|

| Customer Deposits (€bn) | 987 | 412 |

| Loan-to-Deposit Ratio | 78% | 82% |

| Net Interest Margin (Q1 2026) | 1.42% | 1.29% |

| Wealth Mgmt AUM (€bn) | 12.4 | 8.7 |

| YoY Deposit Growth | 12% | 9% |

The Regulatory Wildcard: Wealth Taxes and Capital Flight

The Dutch government’s proposed “vermogensrendementsheffing” (wealth tax) on cash balances above €30,000 threatens to accelerate capital outflows. The tax, set at 31% of a notional 6.17% return (regardless of actual yield), would impose a 1.9% annual levy on idle cash. For a household with €50,000 in savings, that’s €380 per year—enough to deter small-scale investors but not enough to stop high-net-worth individuals from moving assets to Luxembourg or Belgium, where similar thresholds are €100,000.

Luxembourg’s **CSSF** reported a 17% increase in Dutch-domiciled investment funds in 2025, while Belgian banks saw a 22% rise in Dutch retail accounts. The trend is clear: regulatory arbitrage is reshaping Europe’s savings landscape. As **BlackRock (NYSE: BLK)** CEO Larry Fink noted in March, “The next decade of European capital markets will be defined by regulatory fragmentation, not monetary policy.”

“The Dutch wealth tax is a textbook example of unintended consequences. It doesn’t soak the rich—it pushes middle-class savings into neighboring jurisdictions where the tax drag is lower. The losers? Domestic equities and small-cap growth companies that rely on retail capital.”

What Happens When the Dam Breaks?

The €1.2 trillion question is what happens when—if—retail investors finally reallocate. A 10% shift from cash to equities would inject €120 billion into European markets. For context, the entire **European Central Bank’s (ECB)** Pandemic Emergency Purchase Programme (PEPP) totaled €1.85 trillion over two years. The macro impact would be immediate:

- Equity valuations: The **Euro Stoxx 50** could re-rate to 18× forward earnings, a 18.4% upside from current levels, per **Goldman Sachs** estimates.

- Corporate funding: Small-cap companies (**MSCI Europe Modest Cap Index**) would see cost of capital decline by 50-75 basis points, unlocking €25 billion in capex, according to **S&P Global**.

- Inflation: A 1% increase in household equity exposure correlates with a 0.3% rise in consumer spending within 12 months, per **ECB working papers**.

But the timing is everything. If the reallocation coincides with a Fed pivot or a dovish ECB, the effect could be multiplicative. If it happens during a geopolitical shock (e.g., escalation in Ukraine or a U.S. Recession), the result could be a liquidity trap—cash flooding into overvalued assets, only to retreat at the first sign of volatility.

The Actionable Playbook for Investors

For retail investors, the path forward is not binary (cash vs. Equities) but layered. Here is the pragmatic playbook:

- Dollar-cost average into core holdings. A 60/40 split between the **iShares MSCI Europe UCITS ETF (LSE: IEUR)** and **Vanguard Global Aggregate Bond UCITS ETF (LSE: VAGP)** reduces volatility while capturing 80% of the market’s upside. Since 2000, this portfolio has returned 6.8% annualized with a maximum drawdown of 22%.

- Tax-loss harvest. Dutch investors can offset capital gains with losses, but the window closes on December 31. Selling underperforming positions in **ASML (AMS: ASML)** or **Shell (AMS: SHELL)** to offset gains in **ASR Nederland (AMS: ASRNL)** could save €1,200 for every €10,000 in gains.

- Leverage employer matches. Only 34% of Dutch employees contribute to employer-sponsored pension plans, leaving €1.8 billion in unclaimed matching contributions annually. A 5% salary deferral with a 50% employer match yields a 50% instantaneous return—effectively free money.

The Takeaway: The Cost of Waiting Is Already Here

Peter Siks’ warning is not about hypothetical future losses. The cost of inaction is already embedded in household balance sheets, corporate funding costs, and GDP growth. The €1.2 trillion parked in cash is not a neutral asset—it is a drag on economic dynamism, a subsidy to banks, and a missed opportunity for wealth creation.

When markets open on Monday, the **Euro Stoxx 50** will likely test 4,900. The question is not whether it will get there, but whether retail investors will participate in the rally—or watch from the sidelines as their purchasing power erodes. The data is clear: the most expensive mistake is not a subpar investment. It is no investment at all.

For further reading: