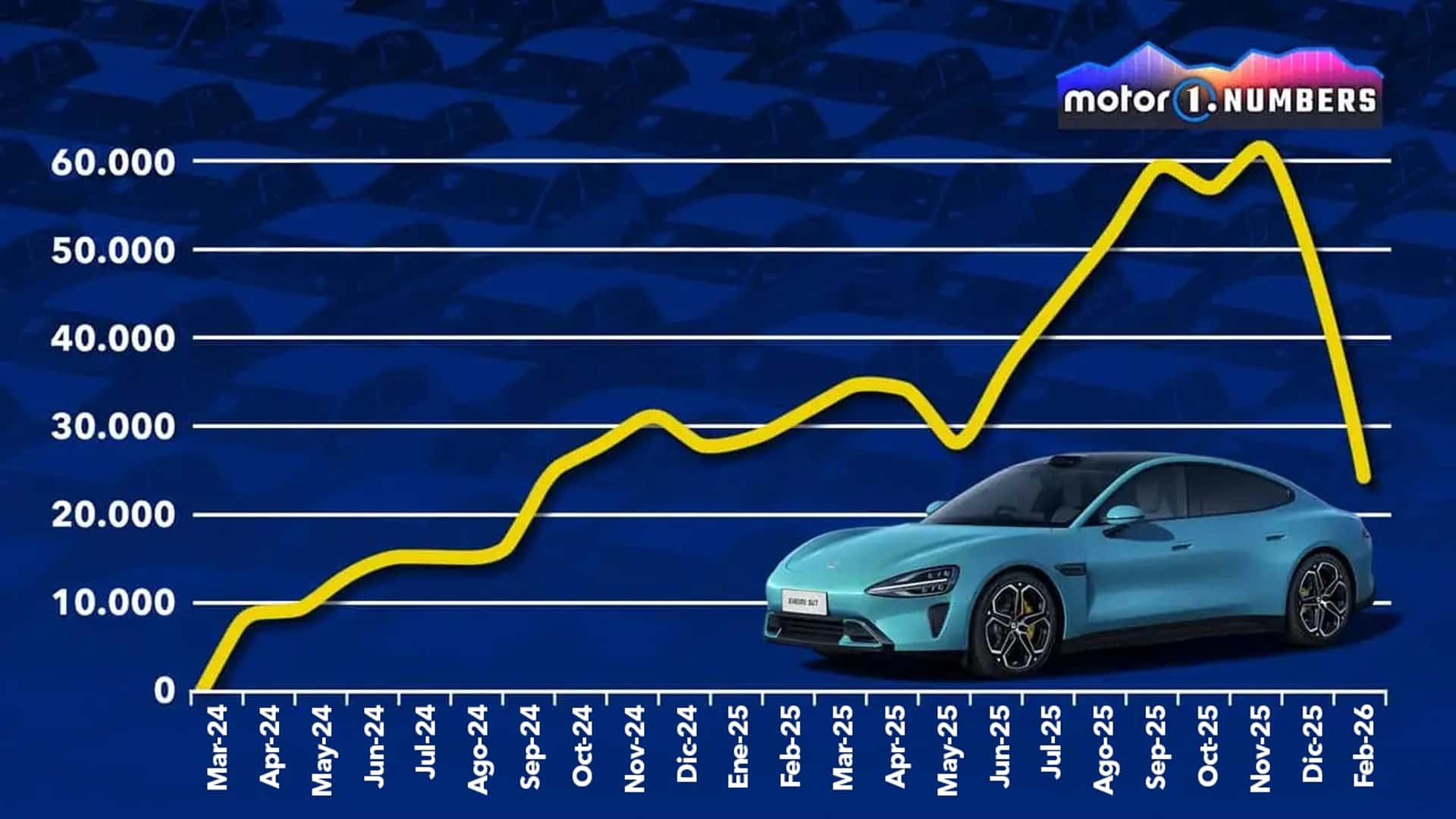

Xiaomi is aggressively scaling its automotive division, leveraging the commercial success of its YU7 model to challenge Tesla’s dominance through deep ecosystem integration. By merging its proprietary HyperOS with high-performance EV hardware, Xiaomi is transitioning from a consumer electronics giant into a vertically integrated mobility powerhouse, redefining the software-defined vehicle (SDV) landscape.

The transition of Xiaomi from a smartphone manufacturer to a serious contender in the electric vehicle (EV) space is no longer a speculative roadmap item. it is a demonstrated market disruption. While the industry spent years debating battery chemistry and range anxiety, Xiaomi pivoted to the real battleground of the late 2020s: the convergence of mobile computing and automotive architecture. The success of the YU7 in the Chinese market serves as a proof-of-concept that the next generation of automotive leaders will not be traditional car companies, but rather computing companies that happen to manufacture chassis.

The HyperOS Convergence: Beyond Simple Infotainment

Most legacy automakers treat the in-car interface as a glorified tablet—a secondary layer of “infotainment” that sits atop a traditional vehicle control unit (VCU). Xiaomi has taken a fundamentally different approach. Through the deployment of HyperOS, the company has achieved a level of vertical integration that makes Tesla’s ecosystem look siloed by comparison.

This isn’t just about mirroring your phone on a dashboard. It is about a unified, low-latency distributed computing environment. When you approach your Xiaomi vehicle, your smartphone, smart home, and car engage in a seamless handshake. The vehicle becomes a mobile node within the user’s personal IoT mesh. We are seeing the implementation of “Human x Car x Home” logic, where the car’s NPU (Neural Processing Unit) can offload non-critical computational tasks to the home’s edge servers or vice versa, optimizing power consumption and processing speed.

This integration creates a massive “moat” of user stickiness. Once a consumer has their entire digital life—from their smart lights to their wearable health data to their vehicle’s driving profile—mapped into a single, cohesive OS, the friction of switching to a competitor like Tesla or BYD becomes exponentially higher. It is the ultimate play for platform lock-in.

The Silicon Battleground: Compute vs. Efficiency

To support this level of ecosystem fluidity, the hardware requirements are staggering. The YU7 and the upcoming SUV lineup rely on a high-bandwidth zonal architecture. Unlike the traditional CAN bus (Controller Area Network) systems used in older vehicles, which are too unhurried for modern sensor fusion, Xiaomi is leveraging automotive-grade Ethernet to handle the massive data throughput required by high-resolution LiDAR and multi-camera arrays.

The core of this capability lies in the vehicle’s SoC (System on a Chip). While Tesla has famously moved toward its own custom silicon for FSD (Full Self-Driving), Xiaomi appears to be leveraging a hybrid approach, utilizing highly optimized third-party automotive SoCs paired with proprietary NPU accelerators designed specifically for the HyperOS kernel. This allows for real-time processing of complex LLM (Large Language Model) queries within the cockpit, enabling a truly conversational AI assistant that understands context, not just voice commands.

| Metric | Xiaomi YU7 (Projected) | Tesla Model Y (2026 Refresh) | Technical Significance |

|---|---|---|---|

| Compute Capacity | 500+ TOPS | ~350-450 TOPS | Essential for Level 3+ autonomy and local LLM execution. |

| OS Architecture | HyperOS (Distributed) | Tesla OS (Siloed/Vehicle-Centric) | Determines ecosystem integration, and latency. |

| Connectivity Standard | V2X + IoT Mesh | V2X + Starlink | Impacts the “Smart Home” integration capability. |

| Sensor Fusion Latency | <10ms | ~15-20ms | Critical for high-speed edge-case maneuvering. |

Security Implications: The Expanded Attack Surface

However, this hyper-connectivity is a double-edged sword. From a cybersecurity perspective, the “Human x Car x Home” model significantly expands the attack surface. In a traditional vehicle, an exploit usually requires physical access or a cellular breach of the vehicle’s specific gateway. In the Xiaomi model, a vulnerability in a low-security IoT device—say, a smart lightbulb or a home security camera—could theoretically serve as an entry point for lateral movement into the vehicle’s network.

As we integrate these systems, the industry must move toward a strict zero-trust architecture for automotive networking. We cannot assume that because a command is coming from a “trusted” paired smartphone, it is inherently safe. The implementation of end-to-end encryption between the mobile device and the vehicle’s VCU is non-negotiable, yet the complexity of managing these keys across millions of heterogeneous IoT devices remains a massive hurdle for engineers.

“The challenge for legacy OEMs isn’t the battery; it’s the software-defined vehicle (SDV) architecture. Xiaomi isn’t building a car; they are building a node in a distributed computing network that happens to have wheels. The security implications of this convergence cannot be overstated.” — Senior Cybersecurity Analyst, Automotive Systems.

We must also consider the implications of over-the-air (OTA) updates. While Tesla pioneered the concept, Xiaomi’s ability to push updates that affect not just the car, but the interaction between the car and the home, introduces a layer of systemic risk. A flawed update could, in theory, disrupt a user’s entire physical and digital environment simultaneously.

The Scaling Strategy: From Niche to Mass Market

Xiaomi’s roadmap is clear: dominate the mid-to-high-end SUV segment to build brand prestige, then use the economies of scale gained from their smartphone manufacturing to flood the mass market. This is a volume game. By leveraging existing supply chains for semiconductors and battery cells, they can achieve price-to-performance ratios that are difficult for traditional luxury automakers to match.

To understand the depth of the underlying software standards that drive this industry, one should look at the Autoware foundation, which provides the open-source framework many are using to benchmark autonomous capabilities. Xiaomi, however, is clearly steering away from open-source dependency in favor of a closed, proprietary stack to maximize their ecosystem advantage.

The macro-market dynamics suggest that the “chip wars” will soon move from the data center to the driveway. As vehicles demand more NPU power to handle edge computing and real-time sensor fusion, the competition between companies like NVIDIA, Qualcomm, and specialized automotive silicon designers will dictate who wins the next decade of mobility. For Xiaomi, the goal is to ensure that they are not just a customer of this silicon, but a master of its application.

As we monitor the rollout of their new SUV models throughout the remainder of this year, the metric for success won’t just be units sold. It will be the depth of the data loop: how effectively the vehicle learns from the user’s digital habits to provide a predictive, autonomous, and deeply personal driving experience. If they succeed, Tesla may find itself fighting not a car company, but a ubiquitous digital presence that is already inside the consumer’s pocket.

For deeper technical dives into the standards governing these connections, researchers should consult IEEE Xplore or follow the latest hardware analysis on Ars Technica.