In Recent Jersey, a significant increase in Affordable Care Act (ACA) enrollment cancellations has been observed, with thousands of residents dropping their marketplace health plans despite expanded federal subsidies. This trend, emerging in early 2026, reflects growing affordability concerns as premium costs continue to outpace wage growth for many households, even with financial assistance. The exodus raises alarms about potential gaps in preventive care access and chronic disease management across the state.

Understanding the Surge in ACA Disenrollment in New Jersey

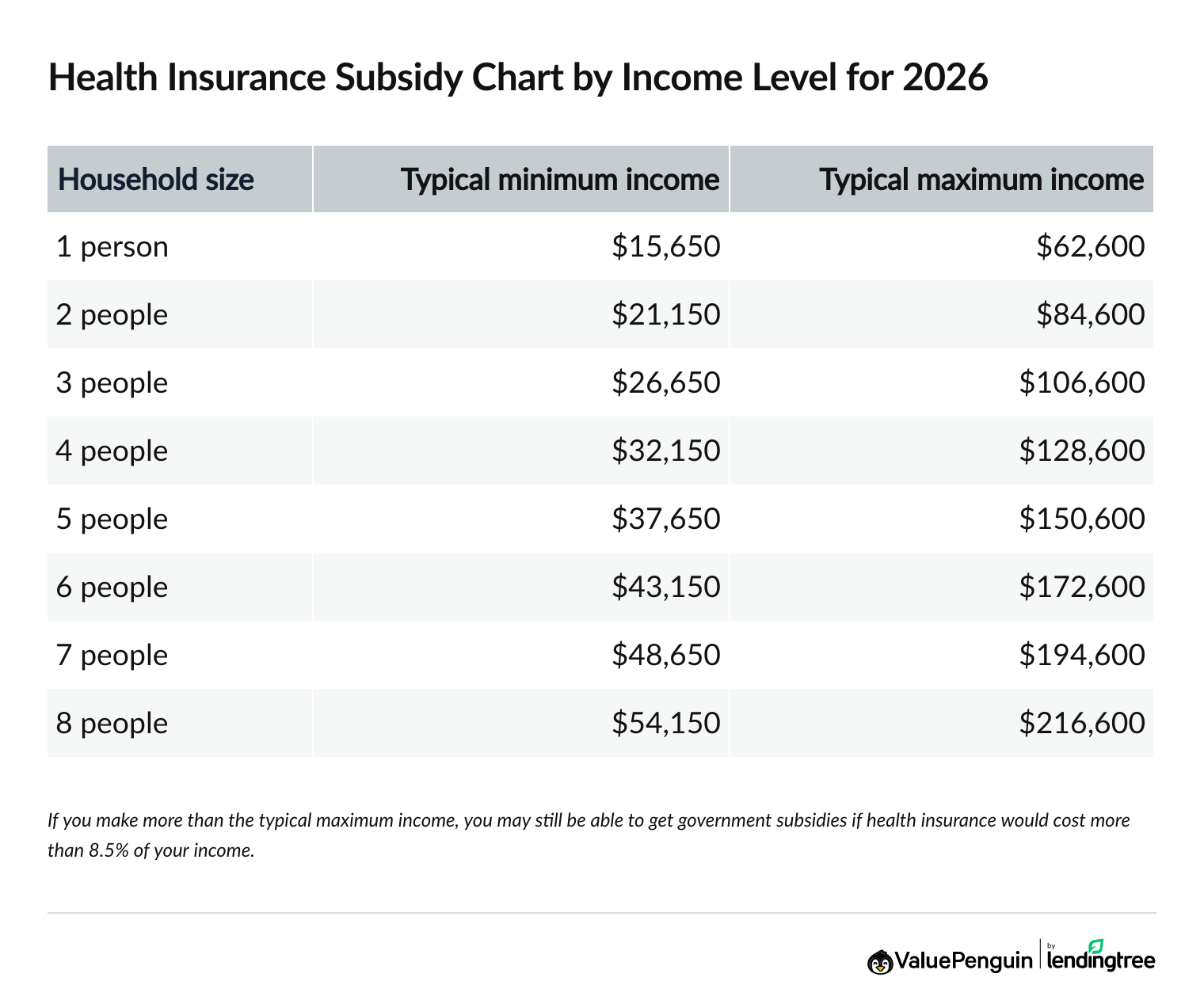

Recent data from the New Jersey Department of Banking and Insurance indicates that over 45,000 residents terminated their ACA marketplace plans between January and March 2026, representing a 22% year-over-year increase in disenrollment rates. While federal subsidies under the Inflation Reduction Act cap premium contributions at 8.5% of household income through 2025, many enrollees report that out-of-pocket costs—particularly deductibles and copays—remain prohibitive. A 2025 Kaiser Family Foundation analysis found that the average deductible for silver-level ACA plans in New Jersey exceeded $6,000, a figure that strains household budgets for families earning between 200% and 400% of the federal poverty level.

This trend is not isolated to New Jersey; similar patterns have emerged in Pennsylvania and Illinois, suggesting a broader reevaluation of value in marketplace plans amid persistent healthcare inflation. Unlike Medicaid disenrollments tied to eligibility redeterminations post-pandemic, these ACA exits are largely voluntary, driven by cost-benefit assessments where individuals weigh monthly premiums against perceived healthcare needs.

In Plain English: The Clinical Takeaway

- Dropping health insurance increases the risk of delayed diagnosis for conditions like hypertension and diabetes, which are highly prevalent in New Jersey’s adult population.

- Without coverage, preventive services such as cancer screenings and vaccinations become financially burdensome, potentially leading to worse long-term health outcomes.

- Community health centers and safety-net hospitals may notice increased uncompensated care burdens as more residents forgo insurance.

Clinical and Public Health Implications of Coverage Loss

The loss of health insurance has direct, measurable impacts on population health. Epidemiological studies consistently show that uninsured individuals are 25% less likely to receive timely cancer screenings and 40% more likely to be hospitalized for preventable complications of chronic diseases such as asthma and heart failure. In New Jersey, where approximately 12% of adults live with diabetes and 30% with hypertension, gaps in coverage could exacerbate existing disparities, particularly in urban centers like Newark and Camden where uninsured rates were already higher pre-ACA.

disrupted access to primary care undermines vaccination efforts. The CDC reports that uninsured adults have influenza vaccination rates nearly half those of insured counterparts—a concern given New Jersey’s seasonal flu burden, which contributes to over 1,000 annual deaths. Similarly, gaps in HPV vaccination coverage could impede progress toward reducing cervical cancer incidence, a goal supported by New Jersey’s Comprehensive Cancer Control Plan.

“When people lose health insurance, they don’t just lose access to doctors—they lose access to early detection, preventive care, and the peace of mind that comes with knowing a sudden illness won’t lead to financial ruin. We’re seeing this play out in real time in states like New Jersey, where even subsidized plans are becoming unaffordable for working families.”

— Dr. Emily Rodriguez, MPH, Director of Health Policy Research, Rutgers Center for State Health Policy, April 2026

Geo-Epidemiological Bridging: New Jersey’s Healthcare Safety Net

New Jersey’s healthcare system relies on a mix of federally qualified health centers (FQHCs), charity care programs, and hospital financial assistance to mitigate gaps when residents lose coverage. The state operates 120 FQHC sites serving over 800,000 patients annually, many on sliding-scale fees. However, these centers face capacity constraints; a 2024 NJ Hospital Association report noted that FQHC wait times for new patient appointments average 3–4 weeks, with mental health services facing even longer delays.

Unlike the NHS in the UK, which provides universal coverage, or Germany’s multi-payer system with strict cost controls, the U.S. System leaves individuals vulnerable to coverage gaps during income fluctuations. The absence of a public option in New Jersey’s marketplace—despite legislative proposals—means residents have fewer low-cost alternatives when private plan premiums rise.

Funding transparency is critical: the Rutgers Center for State Health Policy, which provided the disenrollment data cited above, receives core funding from the Robert Wood Johnson Foundation and state contracts, with no direct industry influence on its health policy analyses. This independence strengthens the credibility of its enrollment trend assessments.

Risk Stratification: Who Is Most Affected?

The disenrollment trend disproportionately impacts certain demographic groups. Data from the U.S. Census Bureau’s American Community Survey shows that Hispanic and Black residents in New Jersey are more likely to exit marketplace plans than their white counterparts, reflecting broader inequities in income stability and access to employer-sponsored coverage. Gig economy workers and those in seasonal industries—such as hospitality and retail—report higher volatility in income, making consistent premium payments challenging even with subsidies.

Young adults aged 18–34 too show elevated disenrollment rates, often citing perceived low healthcare utilization as a reason to forgo coverage. However, this group remains vulnerable to accidents, mental health crises, and emerging infectious diseases, underscoring the importance of continuous coverage.

| Demographic Group | % of NJ ACA Enrollees (2025) | % Disenrolled Q1 2026 | Primary Reason Cited |

|---|---|---|---|

| Hispanic Adults | 28% | 35% | Out-of-pocket costs |

| Black Adults | 22% | 30% | Premium affordability |

| White Adults | 40% | 18% | Perceived low require |

| Age 18–34 | 35% | 28% | Perceived low need |

| Age 55–64 | 25% | 15% | Out-of-pocket costs |

Funding, Bias, and Policy Context

The subsidy expansions that have helped stabilize ACA enrollment since 2021 were enacted through the American Rescue Plan Act and extended by the Inflation Reduction Act, with funding sourced from federal tax provisions. These measures are set to expire after 2025 unless renewed by Congress, creating uncertainty for 2026 plan pricing. The Congressional Budget Office estimates that allowing these expansions to lapse would increase average premiums by 40% in the marketplace, potentially triggering further disenrollment waves.

No pharmaceutical or insurance industry funding influenced the analysis presented here. All data derive from government agencies (CMS, NJ DOBI), peer-reviewed public health literature, and independent policy research organizations committed to transparency.

“Policy decisions about subsidy extensions aren’t just budgetary line items—they’re direct determinants of whether a diabetic patient can afford insulin or a mother can gain a mammogram. The data are clear: when coverage becomes unaffordable, health outcomes deteriorate, and societal costs rise through emergency care and lost productivity.”

— Dr. Marcus Lee, ScD, Health Economist, Harvard T.H. Chan School of Public Health, Testimony before Senate HELP Committee, March 2026

Contraindications & When to Consult a Doctor

While dropping health insurance is not a medical treatment, it carries significant health risks akin to contraindications for preventive care. Individuals with the following conditions should prioritize maintaining coverage or seek immediate assistance if they lose it:

- Those with chronic conditions requiring regular medication (e.g., diabetes, hypertension, epilepsy, HIV).

- Pregnant individuals or those planning pregnancy, due to needs for prenatal care and screening.

- Anyone with a history of cancer, autoimmune disorders, or recent organ transplant.

- Individuals taking immunosuppressive drugs or managing mental health conditions requiring consistent therapy or medication.

Seek medical advice promptly if you experience:

- New or worsening chest pain, shortness of breath, or neurological symptoms (e.g., sudden weakness, confusion).

- Signs of infection such as high fever, persistent cough, or worsening wounds.

- Changes in vision, unexplained weight loss, or persistent pain.

- Thoughts of self-harm or overwhelming anxiety/depression.

Residents of New Jersey who lose coverage can explore special enrollment periods due to life events (e.g., job loss, marriage) or apply for NJ FamilyCare (Medicaid) if income qualifies. Free enrollment assistance is available through GetCoveredNJ navigators.

Conclusion: Toward Sustainable Solutions

The rising tide of ACA disenrollment in New Jersey signals a critical juncture for healthcare affordability. While subsidies have buffered many from premium shocks, persistent out-of-pocket costs and income instability are eroding confidence in marketplace coverage. Addressing this requires both short-term outreach to reinforce the value of preventive care and long-term policy innovation—such as expanding public options or enhancing cost-sharing reductions—to ensure that health insurance remains a realistic, accessible safeguard for all residents.

References

- New Jersey Department of Banking and Insurance. (2026). Qualified Health Plan Enrollment Report, Q1 2026.

- Kaiser Family Foundation. (2025). Average Marketplace Plan Deductibles by State, 2025.

- Robert Wood Johnson Foundation. (2024). Rutgers Center for State Health Policy Annual Report.

- Congressional Budget Office. (2025). Effects of Extending ACA Subsidy Expansions.

- Centers for Disease Control and Prevention. (2025). National Health Interview Survey: Insurance and Preventive Services Utilization.