On July 19, the three major A-share stock indexes were differentiated throughout the day. As of the close, the Shanghai Composite Index rose 0.04%, the ChiNext Index fell 1.77%, and the Shenzhen Component Index fell 0.3%.

In terms of sectors, liquor and finance have recovered one following another, with Huawei Hongmeng concept stocks leading the gains. The new energy track has generally retreated, and photovoltaics and wind power have collectively declined.

Specifically, boosted by the news that Huawei will release Hongmeng 3.0, Hongmeng concept stocks rose strongly during the session. As of the close, Jiulian Technology, Runhe Software 20% daily limit, Tuowei Information, Hengwei Technology daily limit.

Brokerage stocks rose in a straight line late in the session, with the index up regarding 1% following falling as much as 0.5% during the session. CICC rose nearly 5%, and once rose more than 6% during the session.

In terms of individual stocks, Zhongtong Bus closed the down limit with its large orders in the late trading, and the turnover exceeded 5 billion yuan to refresh the historical volume; Ganneng shares of 9 consecutive boards resumed trading at the daily limit, the stock opened in the followingnoon, and finally closed down 5.14%. drop by more than 40%.

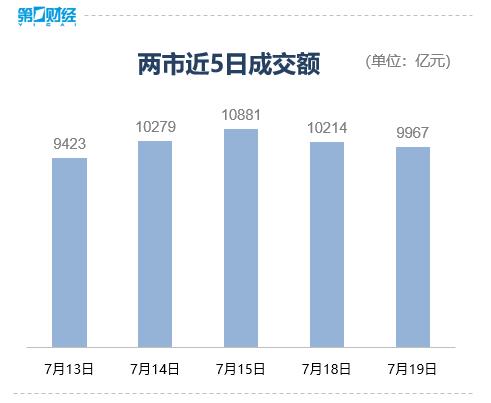

Wind data shows that the unilateral net sales of northbound funds was 9.859 billion yuan throughout the day, a new one-month high; among which, the net sales of Shanghai Stock Connect was 5.795 billion yuan, and the net sales of Shenzhen Stock Connect was 4.063 billion yuan.

【Organization view】

CITIC Securities:As of July 16, the 2021 A-share interim performance report/announcement disclosure rate was 37%. Under the background of structural differentiation, it is recommended to pay attention to the performance of the main line of high prosperity. Among them, the segments with the largest year-on-year and quarter-on-quarter improvement in net profit in the second quarter of 2022 are passenger cars and CXO; There are lithium raw materials, silicon materials, ICL, agrochemicals; other industries with improved profitability also include upstream coal, copper and aluminum, oil and gas, two alkalis, new materials, chemical and biological drugs; midstream military, home appliances, semiconductors, lithium batteries, Photovoltaic, shipping, express, etc.

Galaxy Securities:Under the background of double carbon, the integrated development of communication + energy, the industry resonance ushered in a broad world, the industry continues to expand cutting-edge applications to help the rapid development of energy business, and maintains the “recommended” rating for the communication industry. The marginal improvement in the prosperity of the communication sub-sector is conducive to the stabilization and recovery of valuations, and the certainty of high performance growth in the medium and long term is stronger.

Founder Securities:This cycle of reproductive sows has actually degraded or exceeded expectations. The trend of de-capacity of reproductive sows has become a reality. A new round of pig cycles has begun, and it is currently in the rising channel of a new round of pig cycles. From the investment cycle of the sector corresponding to the pig price cycle, we believe that we are currently in the second stage of the pig cycle investment—capacity reduction and realization. The dual logic of growth will usher in a double-click valuation of “quantity” and “price”, and there is broad room for growth in the sector when volume increases and price rises.