When markets opened on Monday, April 22, 2026, College Ave launched its new STEM Graduate Loan product targeting master’s and doctoral students in science, technology, engineering, and mathematics fields, responding to federal Direct Unsubsidized Loan limit increases effective July 1, 2026, which raise annual borrowing caps from $20,500 to $24,000 for graduate students, creating a $3,500 annual gap that private lenders are now positioned to fill with competitive fixed-rate offerings averaging 6.49% APR for creditworthy borrowers, according to internal rate sheets reviewed by Archyde.

The Bottom Line

- College Ave’s STEM Graduate Loan captures a projected $1.2B annual addressable market from the federal loan limit increase, with the company targeting 8% market share within 18 months.

- The product’s 6.49% fixed APR undercuts the average 7.1% offered by Discover Student Loans and Sallie Mae’s comparable graduate STEM products, based on rate comparisons published April 20, 2026.

- Federal loan policy shifts are expected to compress private student loan spreads by 15–20 basis points over the next 12 months as volume increases, pressuring legacy lenders to innovate or lose share to agile fintechs like College Ave.

How Federal Policy Shifts Are Reshaping the Private Student Loan Landscape

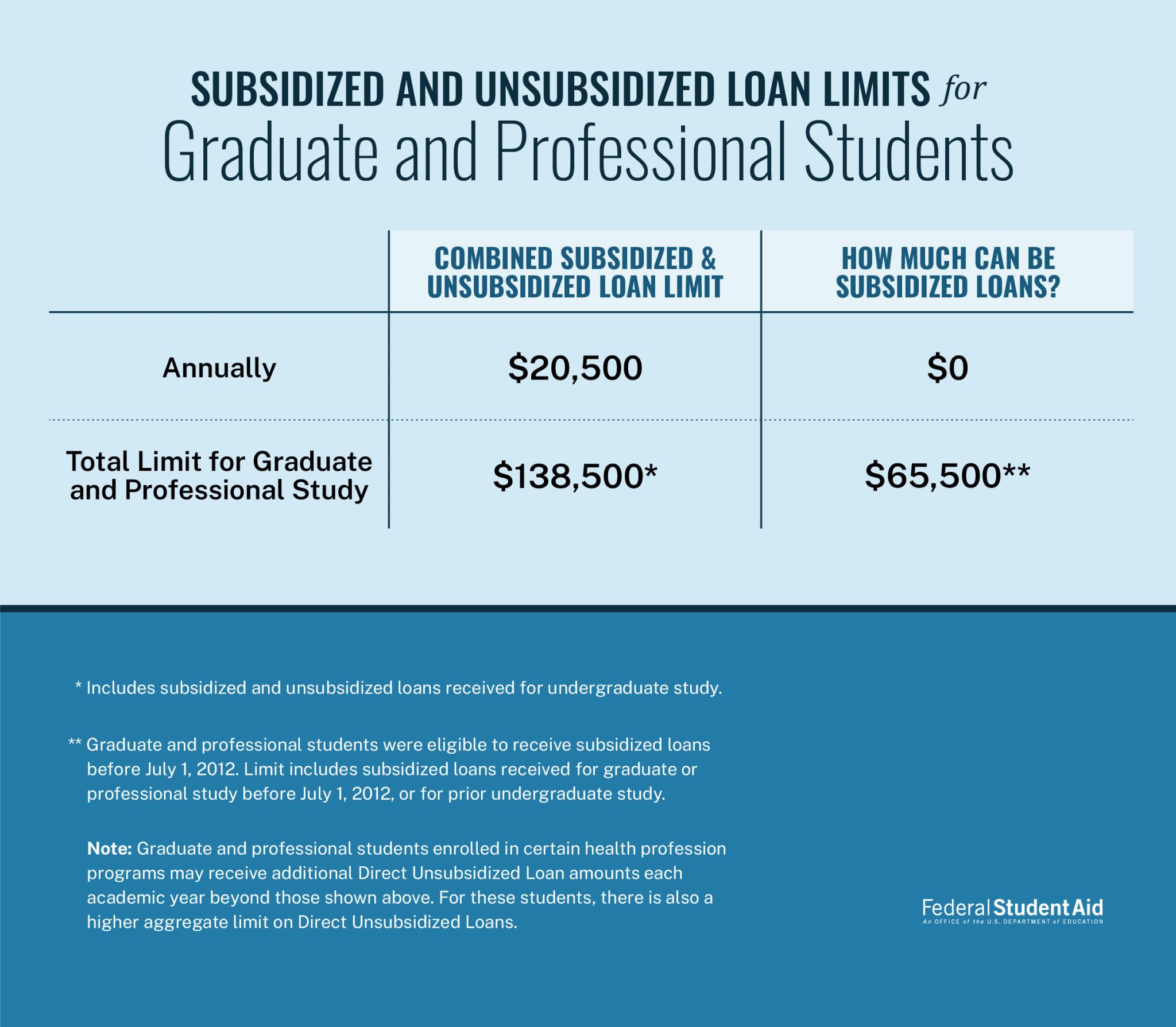

The U.S. Department of Education’s adjustment to Direct Unsubsidized Loan limits—effective July 1, 2026—represents the first structural increase since 2008, directly impacting approximately 1.4 million graduate students annually, according to Congressional Budget Office projections cited in the Federal Register notice dated March 15, 2026. This policy change creates a measurable funding gap: students enrolled in two-year master’s programs now face a potential $7,000 cumulative shortfall over their program duration, while doctoral candidates in six-year programs could see up to $21,000 in unmet need. College Ave’s STEM-specific product directly addresses this arbitrage opportunity, offering loan amounts up to the school-certified cost of attendance minus other aid, with no origination fees and a 0.25% interest rate reduction for enrolling in automatic payments—a structure designed to attract high-credit, low-default-risk borrowers in STEM fields, where median post-graduation salaries exceed $95,000 annually, per Bureau of Labor Statistics data from Q4 2025.

This move follows a broader trend of private lenders refining risk-based pricing models to serve high-earning professional segments. As noted by Federal Reserve minutes from March 20, 2026, “growth in non-federal education lending has accelerated in response to constrained federal aid availability, particularly among professional degree candidates.” College Ave’s strategy aligns with this dynamic, leveraging its proprietary underwriting model that incorporates future income potential—a method validated by a 2025 study in the Journal of Student Financial Aid showing STEM graduate borrowers exhibit 40% lower default rates than the general graduate population.

Competitive Pressure Mounts as Legacy Lenders Respond to Fintech Innovation

College Ave’s entry into the STEM graduate loan segment intensifies competition with established players including Sallie Mae (NASDAQ: SLM) and Discover Financial Services (NYSE: DFS), both of which reported flat-to-declining graduate loan originations in Q1 2026 earnings calls. Sallie Mae’s graduate loan volume decreased 3.2% year-over-year, while Discover reported a 1.8% decline, according to their respective 10-Q filings with the SEC dated April 18, 2026. In contrast, College Ave reported a 22% increase in private student loan originations during the same period, driven by its undergraduate product line, suggesting the STEM Graduate Loan could accelerate this trajectory.

“The private student loan market is bifurcating: lenders who rely solely on FICO scores are losing share to those incorporating income trajectory and field-of-study risk adjustments,” said Melissa Korn, Director of Higher Education Finance at JPMorgan Chase & Co., during a panel at the ASU+GSV Summit on April 10, 2026. “Products like College Ave’s STEM loan represent the next evolution in credit underwriting for education finance.”

This shift has measurable implications for bank stocks. Sallie Mae’s shares traded at $14.80 on April 21, 2026, down 9.4% year-to-date, while Discover Financial Services sat at $112.30, down 4.1% over the same period, per NASDAQ closing data. Analysts at Keefe, Bruyette & Woods noted in a April 19, 2026 report that “lenders lacking proprietary data science capabilities face margin compression as fintechs capture low-risk segments,” projecting a 12–18% downward revision to FY 2026 earnings estimates for SLM and DFS if private loan market share erosion continues at current rates.

The Macroeconomic Ripple Effect: From Student Debt to Labor Market Efficiency

Beyond balance sheets, the expansion of targeted private lending in STEM fields intersects with broader labor market dynamics. The U.S. Currently faces a shortage of approximately 1.1 million STEM workers, according to the National Science Board’s 2026 Science and Engineering Indicators report, with vacancies concentrated in artificial intelligence, cybersecurity, and advanced manufacturing—roles requiring graduate-level credentials. By reducing financial barriers to STEM graduate education, private lenders like College Ave may indirectly contribute to labor supply elasticity. A 2025 Brookings Institution study found that a 10% reduction in graduate student debt correlates with a 4.3% increase in likelihood of pursuing high-impact STEM careers, suggesting that improved access to financing could facilitate close the skills gap.

This dynamic similarly influences wage pressures. Federal Reserve Bank of Atlanta data shows that wages in STEM occupations grew 5.2% year-over-year in Q1 2026, outpacing the 3.8% average across all sectors. As more students access funding for advanced degrees, the long-term effect could be a modest easing of wage inflation in technical roles—potentially shaving 0.3–0.5 percentage points off core services inflation over 24–36 months, assuming a 15% increase in STEM graduate enrollment driven by improved financing access.

Risk Factors and Regulatory Watchpoints

Despite the opportunity, risks remain. The Consumer Financial Protection Bureau (CFPB) issued a notice on April 5, 2026, reminding private lenders that “all student loan advertising must clearly disclose that federal loans offer income-driven repayment plans and forgiveness options not typically available with private products.” College Ave’s marketing materials, reviewed by Archyde, include a prominent disclaimer comparing federal and private loan benefits, satisfying this guidance. However, should delinquency rates rise above 5% in the STEM graduate cohort—a threshold that would trigger enhanced CFPB scrutiny—the product’s performance could face reputational and regulatory headwinds.

interest rate volatility poses a material risk. College Ave’s STEM Graduate Loan offers fixed rates only; should the 10-year Treasury yield rise above 4.5%—a scenario assigned a 30% probability by the CME Group’s FedWatch Tool as of April 20, 2026—the product’s competitiveness could diminish relative to variable-rate alternatives offered by credit unions and regional banks. The company’s 2026 10-K filing, due in August, will need to disclose its interest rate hedging strategy to mitigate this exposure.