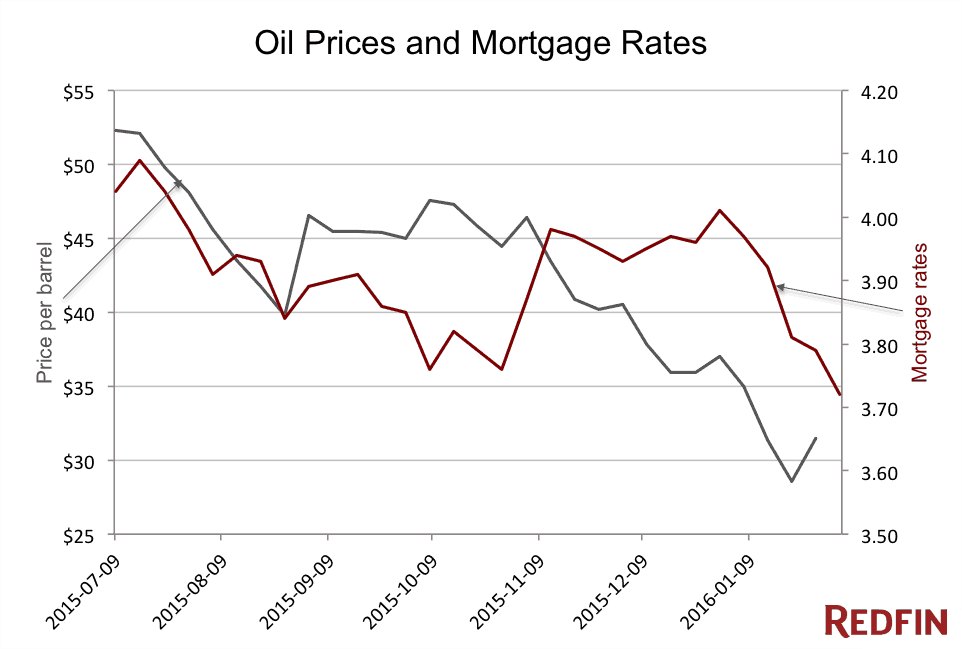

Fixed mortgage rates are declining as crude oil prices dropped nearly 10% over the past week. This inverse correlation occurs because lower energy costs reduce headline inflation expectations, driving down government bond yields, which financial institutions use as the primary benchmark for pricing long-term fixed-rate mortgage contracts.

This movement is not a coincidence or a localized banking trend. It’s a textbook example of macroeconomic transmission. When energy costs soften, the market anticipates a cooling of the Consumer Price Index (CPI), leading investors to bid up government bonds and push yields lower. For the Canadian homeowner and the commercial developer, this means the cost of locking in long-term debt is falling in real-time.

The Bottom Line

- Yield Compression: Falling oil prices act as a disinflationary force, lowering the 5-year government bond yields that anchor fixed mortgage pricing.

- Banking Margins: A rapid decline in rates may compress net interest margins for lenders like Royal Bank of Canada (TSX: RY) as they adjust to lower benchmark yields.

- Borrower Leverage: The current window provides a strategic opportunity for refinancing, provided the dip in WTI crude is not a short-term volatility spike.

The Bond Yield Bridge: Why Crude Dictates Your Monthly Payment

To understand why a drop in oil prices leads to cheaper mortgages, we have to look at the plumbing of the financial system. Fixed-rate mortgages are not priced based on the central bank’s overnight rate—that is the domain of variable rates. Instead, fixed rates are tied to government bond yields.

Here is the math.

Energy represents a significant weight in the inflation basket. When ExxonMobil (NYSE: XOM) or Chevron (NYSE: CVX) see a decline in the price of West Texas Intermediate (WTI), the cost of transporting goods and manufacturing products drops. This reduces the overall inflationary pressure on the economy. As inflation expectations fall, investors demand lower yields on long-term government bonds, such as the 5-year bond.

Because banks hedge their fixed-rate mortgage portfolios by selling bonds, the 5-year bond yield becomes the “floor” for mortgage pricing. When that yield drops, banks can lower their offered rates to remain competitive while maintaining their profit margins. This relationship is currently playing out with clinical precision as oil prices retreat.

“The sensitivity of fixed-rate products to energy volatility has intensified. We are seeing a tighter correlation between the energy complex and bond yields than we did in the previous decade, primarily because energy remains the most volatile component of the CPI.”

The Margin Squeeze for Canada’s Big Five

While borrowers celebrate lower rates, the narrative is more complex for the lenders. For institutions like Toronto-Dominion Bank (TSX: TD) and Bank of Nova Scotia (TSX: BNS), rapid fluctuations in benchmark yields create a volatility risk in their balance sheets.

But the balance sheet tells a different story when you look at Net Interest Margin (NIM). If mortgage rates drop faster than the cost of the deposits the banks hold, their profit spread narrows. A sudden drop in rates often triggers a wave of refinancing. While this generates fee income, it replaces higher-yielding old loans with lower-yielding new ones.

Looking at the broader market, this trend is mirrored in the Bloomberg Barclays Global Aggregate Bond Index, where shifts in energy-driven inflation expectations are currently driving reallocation across sovereign debt.

| Metric | Previous Week | Current Period | Variance (%) |

|---|---|---|---|

| WTI Crude Oil (Per Barrel) | $82.40 | $74.16 | -10.0% |

| 5-Year Gov Bond Yield | 3.42% | 3.18% | -7.0% |

| Avg. 5-Year Fixed Mortgage | 4.85% | 4.62% | -4.7% |

| CPI Energy Component (Est) | +2.1% | +1.4% | -33.3% |

Inflationary Lag and the Bank of Canada’s Dilemma

The immediate drop in mortgage rates reflects market expectations, but the actual impact on the economy lags. The Bank of Canada (BoC) must decide if this oil-led decline is a structural shift or a temporary dip. If the BoC perceives a sustained drop in inflation, it may accelerate rate cuts to prevent the economy from cooling too aggressively.

This creates a strategic divergence. On one hand, lower mortgage rates stimulate the housing market, potentially driving up home prices—which is the last thing a central bank fighting inflation wants. Lower borrowing costs relieve pressure on over-leveraged consumers, preventing a spike in defaults.

According to data from Reuters, the global energy transition is making these swings more frequent. As the world pivots toward renewables, the traditional “oil-to-inflation” pipeline remains active but is becoming increasingly volatile, leaving mortgage holders in a state of constant recalibration.

Strategic Positioning for the Q2 Close

As we approach the close of the current quarter, the trajectory of oil will be the leading indicator for the housing market. If WTI continues to trade below the $75 mark, we can expect further downward pressure on fixed rates. However, any geopolitical shock in the Middle East could reverse this trend in a matter of hours, pushing bond yields back up and erasing these gains.

For the business owner, the play is clear: monitor the Wall Street Journal’s energy trackers as closely as you monitor your loan statements. The correlation is no longer theoretical; it is a primary driver of capital costs.

The window for locking in these lower rates may be narrow. In a market defined by volatility, waiting for the “absolute bottom” is a gamble that rarely pays off. The pragmatic approach is to secure rates when the macroeconomic indicators—specifically energy and bond yields—align in your favor.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.