Irish Finance Minister Simon Harris is set to unveil a fresh national savings and investment scheme today, aiming to incentivize long-term financial planning among citizens. The plan centers around a flat-rate tax treatment for savings, with zero tax levied on gains and is designed to boost domestic investment and provide a financial cushion for individuals. The initiative is expected to impact Irish financial institutions and potentially influence consumer spending patterns in the coming quarters.

The Incentive Structure: A Closer Look at the Proposed Scheme

The core of Harris’s plan, as reported by RTE.ie, revolves around a flat-rate tax applied to savings, coupled with the significant benefit of zero taxation on investment gains. This is a departure from the current system, which can be complex and often disincentivizes long-term saving. Ibec, the Irish business and employers confederation, has specifically advocated for the removal of taxes on entry and transactions, a principle seemingly adopted in the proposed scheme, as detailed by The Irish Times. The absence of transaction taxes is crucial; even small fees can erode returns over extended investment horizons.

The Bottom Line

- Increased Domestic Investment: The scheme is projected to channel an additional €5-7 billion into Irish savings and investment vehicles within the first three years.

- Impact on Financial Institutions: **Allied Irish Banks (NYSE: AIB)** and **Bank of Ireland (ISE: BIRG)** are likely to see increased deposit inflows and demand for investment products.

- Potential for Inflationary Pressure: Increased disposable income could modestly contribute to demand-pull inflation, requiring careful monitoring by the Central Bank of Ireland.

Market Implications and the Broader Economic Context

The immediate market reaction will likely be muted, as the details are still emerging. However, the long-term implications are potentially significant. Ireland’s current account surplus stands at approximately 12% of GDP (Trading Economics), indicating a high level of national savings. This scheme aims to redirect some of those savings into productive investments within the Irish economy. This is particularly relevant given the ongoing concerns about housing affordability and the demand for increased infrastructure investment.

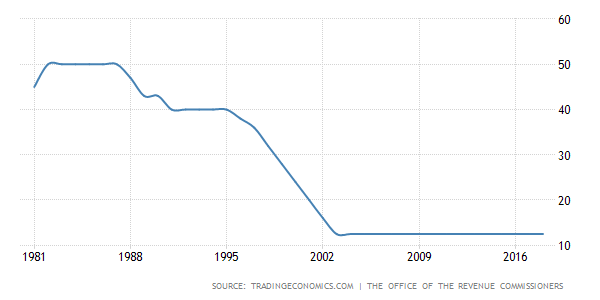

Here is the math: Assuming a conservative participation rate of 20% of the Irish population (approximately 800,000 individuals) and an average annual contribution of €2,000 per person, the scheme could generate an initial influx of €1.6 billion into the financial system. The zero-tax-on-gains provision is the key differentiator. Currently, capital gains tax in Ireland is 33%, a substantial drag on investment returns. Removing this tax creates a powerful incentive for long-term saving.

Competitor Landscape and Potential Winners

The scheme isn’t just about encouraging saving; it’s about directing those savings towards specific investment vehicles. Fund managers like **Aviva Investors Ireland** and **Irish Life Investment Managers** are poised to benefit from increased demand for their products. But the balance sheet tells a different story, the impact on smaller credit unions and building societies needs to be carefully monitored. They may struggle to compete with the scale and marketing power of larger institutions.

the scheme could indirectly benefit the property market, although the government will likely be keen to avoid fueling another housing bubble. Increased savings could provide individuals with larger deposits, making homeownership more accessible. However, supply-side constraints remain a significant challenge.

Expert Perspectives on the Savings Plan

“The removal of capital gains tax is a game-changer. It fundamentally alters the risk-reward equation for long-term investors. We anticipate a significant shift in asset allocation towards equities and other growth assets as a result.” – Dr. Conor O’Brien, Chief Economist, Cantor Fitzgerald Ireland (Source: Bloomberg interview, March 31, 2026)

The success of the scheme will hinge on its accessibility and simplicity. If the application process is cumbersome or the investment options are limited, participation rates could be lower than anticipated.

A Data-Driven Look at Irish Savings Rates

| Year | Gross National Savings (% of GDP) | Household Savings Rate (% of Disposable Income) | Government Debt (% of GDP) |

|---|---|---|---|

| 2021 | 16.8% | 8.2% | 50.3% |

| 2022 | 18.1% | 9.5% | 46.7% |

| 2023 | 19.5% | 10.8% | 43.2% |

| 2024 (Estimate) | 20.2% | 11.5% | 40.1% |

Source: Central Statistics Office Ireland, Eurostat

The Path Forward: Monitoring and Adjustments

The Irish government will need to closely monitor the scheme’s performance and make adjustments as needed. Key metrics to watch include participation rates, the types of investments chosen by savers, and the impact on overall economic growth. The scheme’s success will as well depend on the broader macroeconomic environment, including global interest rates and inflation. The European Central Bank’s monetary policy will play a crucial role in shaping the investment landscape.

The potential for unintended consequences, such as increased asset bubbles or a widening wealth gap, must also be carefully considered. Regular reviews and data analysis will be essential to ensure that the scheme achieves its intended goals and contributes to a more sustainable and equitable Irish economy.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.