What is the cause of the current inflation?

- In 2020, COVID-related lockdowns caused the supply of goods and services to plummet.

- Large budget deficits and an easing of monetary policy have had the effect of stimulate aggregate demand.

- The excess of demand over supply triggered a rise in prices.

- The central banks of developed countries have not reacted because inflation has been low there for decades.

- In 2022, another shock: the supply of grain, oil and gas has been significantly reduced due to the conflict between Russia and Ukraine and the sanctions imposed. Commodity prices have therefore increased.

- Fiscal policy remained expansionary, but monetary policy turned restrictive, which also had an impact on financial conditions.

Graph 1: Central banks – Key rates

Is this the end of the inflationary phenomenon?

- Headline inflation is down. Over the next few months, the liquidation of commodity and energy inventories should help bring it down further.

- However, the path is not yet clear. Recently, lower gas prices in Europe and gasoline prices in the United States have boosted demand. Financial conditions have improved.

- In the medium term, it is difficult to predict how long it will take for this effect of “revenge spending” (phenomenon of increased consumer spending to compensate for restrictions linked to the pandemic) to diminish and for the labor market to begin to recover. weaken.

- In the long term, many are betting on a return to low inflation, low growth, low productivity and low interest rates.

- However, several factors present an upside risk. De-globalization may lead to higher costs of sourcing goods. The green transition might increase demand. Central banks might increase their inflation targets by 2 to 3%.

- A change in psychology can occur. Inflation is the result of decisions made by billions of economic actors. They are influenced by their own inflation expectations which can sometimes be irrational.

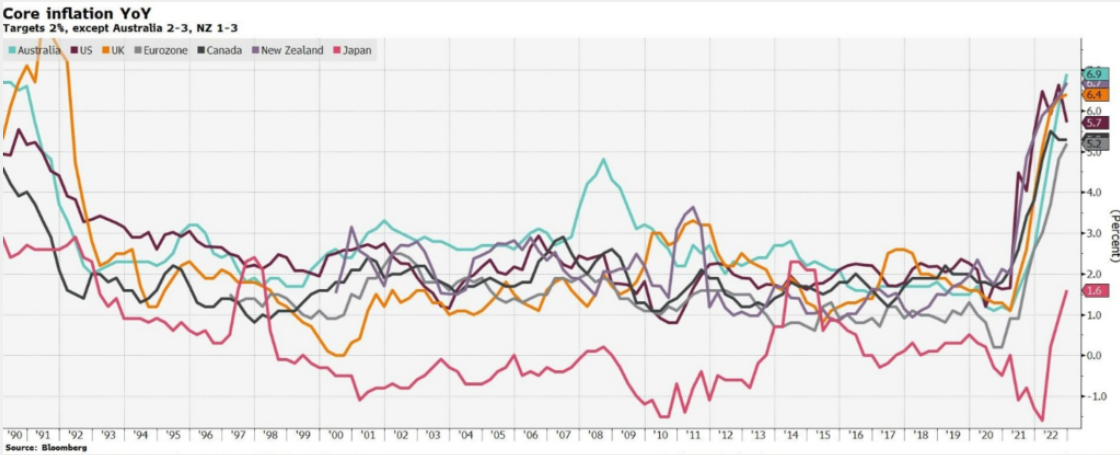

Graph 2: Evolution of core inflation year-on-year

- Source: Bloomberg – February 10, 2023

What use are inflation-indexed bonds today?

- The difference between nominal and real returns represents a measure of inflation expectations: the “breakevens”.

- Throughout the current episode of inflation, market participants continued to believe that central banks would soon hit their 2% targets. Indeed, 5-year breakevens in the United States and the euro zone have never exceeded 3.8%. A figure that seems very underestimated compared to an average increase in the consumer price index (CPI) of more than 7% over the past year and a half.

- Inflation-linked bonds outperform nominal bonds when realized inflation is above breakeven at the time of purchase. If you bought a US 5-year inflation-linked bond on January 1, 2021, the total return to date would be more than 0%, compared to around -9% for a nominal 5-year bond.

- The yield of inflation-linked bonds depends on their actual yield, as well as the impact of inflation (CPI) on the principal amount of the bond and on its coupon.

- Both real and nominal yields have increased significantly. Although breakevens generally decline in the contraction phase of an economic cycle, rates at 2.2% and 2.3% for 10-year inflation-linked bonds might still be underestimated.

- Even if the worst is over, inflation-indexed bonds can act as a hedge for a bond portfolio.

Chart 3: 10-year break-evens

- Source: Bloomberg – February 10, 2023