Inflation did not merely stay stubborn in May. It reminded Washington, Wall Street and anyone pricing a starter home that the United States is still living in an economy where relief can appear in headlines long before it reaches a monthly payment.

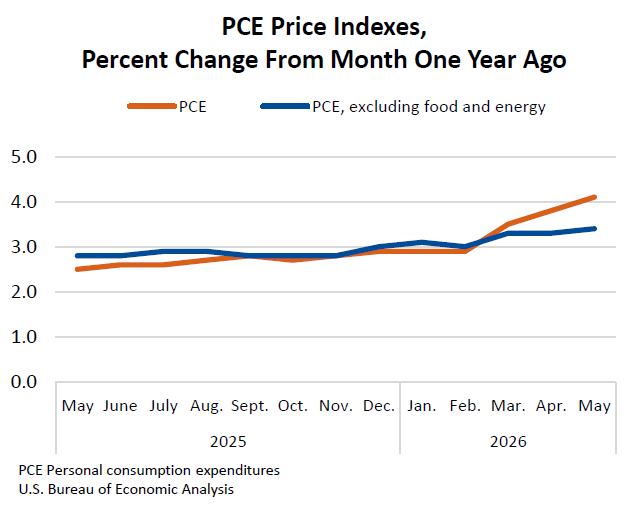

Data released by the U.S. Bureau of Economic Analysis on June 25, 2026, showed the personal consumption expenditures price index, the Federal Reserve’s preferred inflation gauge, rose 0.4 percent from April and 4.1 percent from a year earlier. Core PCE, which strips out food and energy, rose 0.3 percent on the month and 3.4 percent on the year. Personal income and disposable personal income each increased 0.7 percent, while consumer spending also advanced 0.7 percent.

That combination matters because it keeps two stories alive at once. Households are still spending, which argues against recession panic. But prices are still climbing fast enough to make any quick turn toward cheaper credit look harder to justify. For buyers already dealing with the affordability strain Archyde tracked in the Senate’s recent housing-supply push, this is the kind of report that extends the waiting game rather than ending it.

The Fed’s inflation problem is no longer theoretical

For months, investors kept looking for a cleaner glide path back toward the Fed’s 2 percent target. May’s numbers do not offer one. Headline PCE has now moved back above 4 percent, while core inflation remains far enough above target to keep policymakers cautious even if growth cools later in the summer.

That helps explain why the policy conversation has shifted from when cuts begin to whether officials can afford to wait longer, or even tighten again if price pressure spreads. Archyde’s earlier look at the Fed’s hold-with-a-warning stance already captured that tension. May’s report hardens it. When both income and spending keep rising, central bankers can argue the economy still has enough momentum to absorb restrictive borrowing costs.

Why mortgage relief still feels out of reach

Housing remains the clearest everyday transmission mechanism for this inflation story. Freddie Mac’s Primary Mortgage Market Survey listed the average 30-year fixed mortgage at 6.49 percent as of June 25, 2026, with the 15-year fixed rate at 5.84 percent. Those are not emergency-level rates, but they are still high enough to punish marginal buyers, especially after years of elevated home prices.

That is why May’s inflation release lands awkwardly for households that had started to imagine a gentler second half of the year. Even if mortgage rates drift lower week to week, lenders and bond markets still price in the broader inflation regime. A Fed that cannot credibly pivot to easier policy is not a Fed that delivers fast affordability relief. The result looks a lot like the market Archyde described in its recent first-time-buyer affordability snapshot: ownership is technically possible, but increasingly selective and expensive.

| Indicator | May 2026 reading | Why it matters |

|---|---|---|

| PCE price index | 0.4% month over month, 4.1% year over year | Headline inflation moved back above 4%, making fast policy easing harder to defend. |

| Core PCE | 0.3% month over month, 3.4% year over year | Underlying inflation is still running well above the Fed’s 2% target. |

| Disposable personal income | Up 0.7% | Household income growth is helping consumers keep spending despite higher prices. |

| Real consumer spending | Up 0.3% | Demand has not weakened enough to force an immediate policy rethink. |

| Freddie Mac 30-year fixed mortgage | 6.49% | Borrowing costs remain high enough to keep affordability under pressure. |

Consumers are still spending, but the cushion is thinning

BEA said personal saving fell to a 3.0 percent saving rate in May. That is not collapse territory, but it is a useful warning light. Consumers are still moving money through the economy, yet they are not doing it from a position of abundant slack. If inflation stays elevated while financing costs remain high, households may keep spending in the short term and still feel poorer in the process.

That is a key distinction for investors and policymakers. Strong spending does not automatically signal healthy confidence. Sometimes it reflects households absorbing higher prices because essentials, travel, healthcare and debt payments do not wait for better policy timing. It is the same reason a weekly dip in mortgage rates, like the one Archyde noted in Freddie Mac’s earlier June update, can feel helpful without changing the bigger affordability math.

What to watch before the next policy turn

The next test is not whether one report looked hot. It is whether the summer data confirm that May was part of a broader reacceleration. If energy pressure fades, goods prices settle and services inflation cools, officials may regain room to wait patiently. If not, the market will have to price a longer stretch of restrictive policy and a slower path toward mortgage relief.

For now, the cleanest reading is the least comforting one: incomes are holding up, spending is holding up, and inflation is still running hot enough to keep the Fed boxed in. That is manageable for the broader economy. It is much less manageable for households still trying to buy, refinance or plan around the idea that cheaper money is just around the corner.