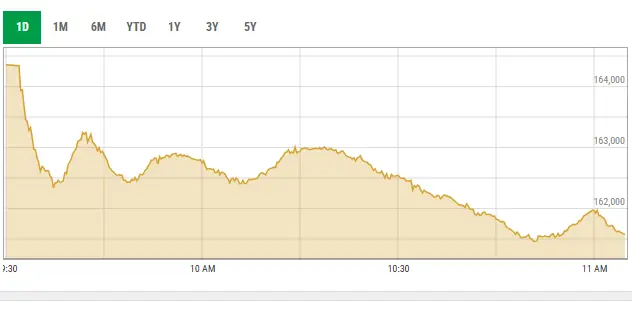

The KSE-100 index of the Pakistan Stock Exchange (PSX: KSE100) declined 3,449.98 points (2.08%) on Thursday, closing at 162,373.89. The downturn was driven by disappointing corporate earnings, Brent crude prices reaching $126.41 per barrel, and reports that Etisalat (ADX: ETT) is reviewing its Pakistani telecom investments.

This volatility is not merely a temporary correction. This proves a systemic reaction to a convergence of geopolitical instability and domestic fiscal fragility. When a primary foreign investor signals a portfolio “optimization” while energy costs surge, the market ceases to trade on fundamentals and begins trading on fear. For institutional investors, the current environment represents a spike in the emerging market risk premium that cannot be ignored.

The Bottom Line

- Energy Vulnerability: Brent crude’s 7.1% increase to $126.41 exacerbates Pakistan’s current account deficit and fuels imported inflation.

- FDI Instability: Etisalat’s (ADX: ETT) strategic review of its telecom exposure threatens to trigger a broader exit of Gulf-based capital.

- Margin Compression: Successive interest rate hikes by the State Bank of Pakistan are aggressively eroding corporate EBITDA and depressing P/E ratios.

The Oil Shock and the Current Account Deficit

The most immediate catalyst for the sell-off is the volatility in the energy complex. Brent for June delivery increased 7.1% to $126.41 per barrel, while West Texas Intermediate rose 3.4% to $110.31. For a net energy importer like Pakistan, these figures are not just numbers—they are a direct hit to foreign exchange reserves.

Here is the math: every $10 increase in the price of a barrel of oil significantly expands the trade deficit, putting downward pressure on the Pakistani Rupee. This creates a feedback loop where a weaker currency increases the cost of imports, which in turn drives domestic inflation higher. As the Bloomberg Terminal often highlights in emerging market analysis, energy shocks typically trigger an immediate “flight to quality,” where investors move capital from frontier markets to the US Dollar or gold.

The geopolitical trigger—Donald Trump’s warnings regarding a blockade of Iranian ports—has introduced a layer of unpredictability that equity markets loathe. When the risk of military strikes enters the equation, the “risk-off” sentiment becomes the default setting for global fund managers.

Etisalat’s Portfolio Review: A Signal for FDI Flight

While oil prices provided the spark, the reports regarding Etisalat (ADX: ETT) provided the fuel. The UAE-based telecom giant is reportedly reviewing its exposure to Pakistan’s telecom sector. In the lexicon of corporate strategy, “portfolio optimization” is often a euphemism for de-risking or divestment.

But the balance sheet tells a different story. The telecom sector in Pakistan has struggled with stagnant Average Revenue Per User (ARPU) and rising operational costs. If Etisalat (ADX: ETT) decides to reduce its stake, it could create a domino effect among other Gulf Cooperation Council (GCC) investors who view the UAE’s movements as a bellwether for regional stability.

“In frontier markets, the exit of a cornerstone investor is rarely an isolated event. It often signals a shift in the perceived risk-reward ratio for the entire sector, leading to a liquidity crunch as other institutional players rush for the exit.”

This potential exit coincides with a broader trend of capital flight from markets where the cost of doing business—measured by electricity tariffs and bank borrowing rates—has become unsustainable. The Reuters reporting on regional trade indicates that high input costs are now the primary headwind for industrial growth in South Asia.

The Interest Rate Trap and Corporate EBITDA

The domestic narrative is dominated by the State Bank of Pakistan’s aggressive monetary tightening. While intended to curb inflation, the resulting interest rate hikes have created a “debt trap” for many listed companies. High borrowing costs are directly eating into net profit margins, leading to the “disappointing earnings” cited by market analysts.

When interest expenses rise, the interest coverage ratio—a key metric for solvency—drops. For companies with high leverage, In other words less capital for CapEx and lower dividends for shareholders. The market is rerating these companies with lower Price-to-Earnings (P/E) multiples.

| Metric | Value (April 30, 2026) | Change/Status |

|---|---|---|

| KSE-100 Closing Level | 162,373.89 | -2.08% |

| Intraday Low | 160,391.18 | -2.11% from close |

| Brent Crude (June) | $126.41 | +7.1% |

| WTI Crude | $110.31 | +3.4% |

The impact extends beyond the stock ticker. High energy tariffs and expensive credit are suppressing consumer spending. As the International Monetary Fund (IMF) continues to mandate fiscal discipline and the removal of subsidies, the transition period is proving painful for the private sector. Business owners are facing a dual squeeze: rising operational costs and falling demand.

The Path Forward: Recovery or Prolonged Bear Market?

The 3,000-point plunge is a stark reminder that the Pakistan Stock Exchange (PSX: KSE100) remains highly sensitive to external shocks. For a recovery to materialize, the market requires two things: a stabilization of global energy prices and a clear signal from the government that the cost of doing business will be managed through structural reforms rather than just monetary tightening.

Investors should monitor the upcoming quarterly guidance from the banking and energy sectors. If the EBITDA margins continue to contract, the bears will maintain control. However, if the World Bank or other multilateral lenders announce new support packages to stabilize reserves, we may see a tactical rebound.

For now, the pragmatic play is caution. The market is pricing in a high-risk environment, and until the geopolitical tension in the Middle East eases, the PSX will likely remain in a state of high volatility.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.