2024-03-14 08:26:00

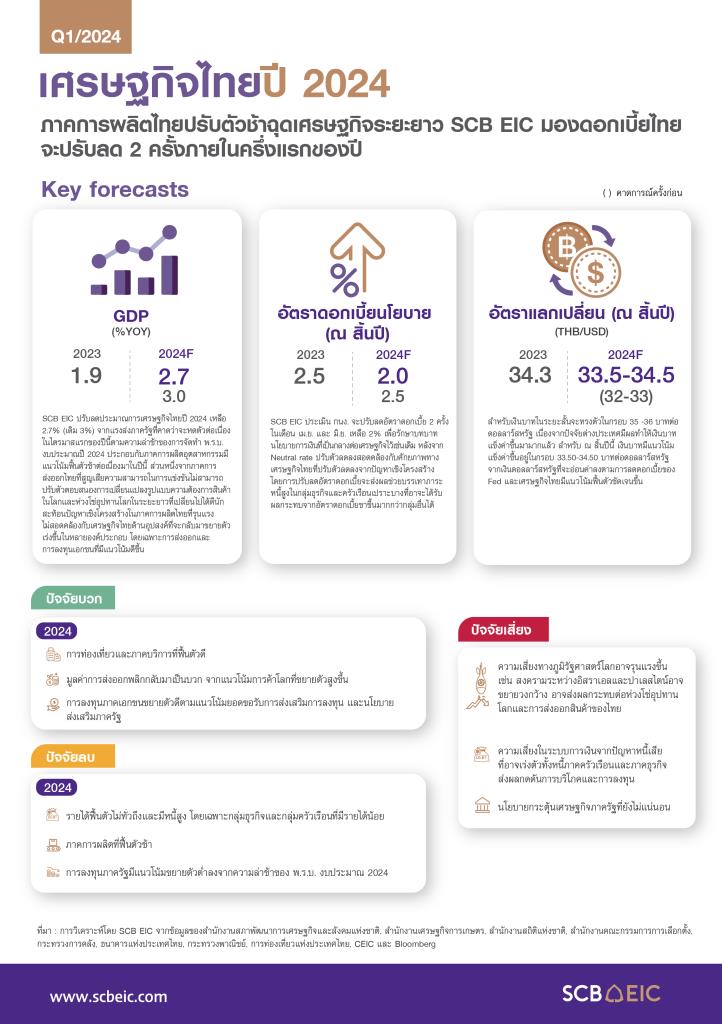

SCB EIC cuts this year’s GDP target to 2.7% from the original 3% due to delays in The Budget Expenditure Act for 2024 expects the MPC to gradually reduce the policy interest rate to 2% within the first half of this year.

Center for Economic and Business Research The Siam Commercial Bank (SCB EIC) lowered its economic forecast for 2024 to 2.7% (originally 3%), although the overall Thai economy in 2024 is likely to continue to recover. Driven by tourism and the service sector as well as other demand-side economies that have returned to accelerate expansion in many components. Especially exports and private investment are likely to improve. But government momentum will continue to shrink in the first quarter from the delay in enacting the Budget Act for 2024, along with the problem of high accumulated inventory from last year that will not be able to be resolved quickly. Partly from structural problems in the Thai manufacturing sector. Especially the Thai export sector has lost its competitiveness. It will be an important factor causing the Thai industrial sector to continue to recover slowly this year.

As for Thai inflation which has continued to be negative for several months, SCB EIC assesses that Thailand is not yet facing deflation. Inflation will return to positive from May as the energy price assistance measures will end. Especially the price of oil in the country will begin to increase. In addition, there is also a high risk of inflation amid the risk of global supply chain disruptions from the Red Sea situation. climate change Including export control policies of some countries that may cause the prices of some agricultural products to increase, such as rice and sugar. General inflation in the second half of the year will then accelerate back to touching the inflation range. SCB EIC estimates general inflation. and core inflation in 2024 are at 0.8% and 0.6%, respectively.

Mr. Somprawin Manprasert, Deputy General Manager Chief Executive Officer, Economic Intelligence Center (EIC) Group and Deputy General Manager Chief Executive Officer Corporate Strategy Group Siam Commercial Bank said that in the long term, the structural problems in Thailand’s manufacturing sector that have become more severe will pressure the potential of the Thai economy to decrease from past estimates. SCB EIC estimates the potential of the Thai economy in the pre-Covid period (2017 – 2019). is at the level of 3.4%, while the long-term potential of the Thai economy has decreased to 2.7% from the original 3%, estimated as of December 2023, aggravating the long-term growth trend of the Thai economy that was already in a downward direction.

The main reasons are: 1) Thailand’s total factor productivity is continually falling, partly due to the problem of declining Thai labor productivity and many government regulations that are obstacles to doing business. 2) Capital factor ) of Thailand which tends to decrease from the proportion of investment in the country which has decreased by more than half to approximately 24% of GDP in the last 2 decades and Thailand’s ability to attract foreign investment (FDI) is lower when compared Countries in the ASEAN region and 3) labor force factors (Labor) that tend to decrease due to entering a rapidly aging society.

SCB EIC estimates that the Monetary Policy Committee (MPC) will gradually reduce the policy interest rate from the current level of 2.5%.

to 2% within the first half of this year To maintain the role of neutral monetary policy towards the economy as before following recalibrating the monetary policy mechanism from more severe structural factors in the production sector and evaluating the implications on the interest rate level that is appropriate for the long-term growth of the Thai economy (Neutral rate) which is lower, SCB EIC estimates that Thailand’s Neutral rate has dropped to around 2.1% (from the previous level of 2.5%). This interest rate cut is in addition to adjusting the stance of monetary policy to suit. The changing structure of the Thai economy has caught up with the situation. It will still have an effect in relieving the high debt burden. Especially vulnerable businesses and households may be more affected by rising interest rates than other groups. Including adding another positive factor to confidence in the Thai economy amidst government sector momentum that is still stuck this year.

As for the baht value in the short term, it will remain stable in the range of 35-36 baht per US dollar. Because foreign factors have already made the baht stronger, the baht at the end of the year tends to strengthen in the range of 33.50-34.50 baht per US dollar. from the US dollar which will depreciate following the Fed’s interest rate reduction and the Thai economy is likely to recover more clearly.

looking forward Thailand faces major challenges due to structural problems in the industrial production sector. Although production in 2024 is likely to return to expansion due to the momentum of consumer products recovering in line with demand both domestically and abroad. But the production of Thai industrial products is still very much tied to the old supply chain. In addition, the Thai economy is very connected to the Chinese economy and the Chinese production chain in the midst of global geopolitical trends. Including the ability of the Thai manufacturing sector to adapt to the new global production chain and the slowly changing patterns of product demand in the world market. As a result, increasing the competitiveness of the Thai export sector is still quite limited. This is reflected in the share of Thai export sales in the world market that has remained close to the same throughout the decade.

Therefore, the adjustment of the Thai industrial sector to be in line with the trend of sustainability. Upgrading capabilities in technology development and managing the supply chain to be more flexible To be able to connect and become part of the new global supply chain. Therefore it is urgently needed.

As for the world economy in 2024, it is likely to grow 2.6%, similar to last year. The view improved from good momentum. in the last quarter of 2023 and economic activity that continued to expand well at the beginning of this year with activities in the service sector expanding at an accelerated pace Meanwhile, activity in the manufacturing sector has begun to expand from a continuous contraction. In addition, the world economy will receive support from global trade that is likely to improve and global inflation to slow down. But there is still pressure from the effects of high interest rates and conflicts.

Protracted geopolitics and global supply chain problems from transportation problems in the Red Sea and the dry Panama Canal.

Central banks of major economies will begin adjusting the direction of monetary policy in the second quarter of this year. The US Federal Reserve will cut interest rates 3 times, totaling 75 BPS, while the European Central Bank and the Bank of England will cut interest rates 4 times, totaling 100 BPS, in line with the direction of inflation that has slowed down. The Bank of Japan is likely to raise the policy interest rate 2 times, totaling 20 BPS, which will end the negative interest rate policy. Meanwhile, the People’s Bank of China will continue to use loose monetary policy to support the economy.

1710410188

#SCB #EIC #cuts #years #GDP #expecting #MPC #cut #interest #rates #year