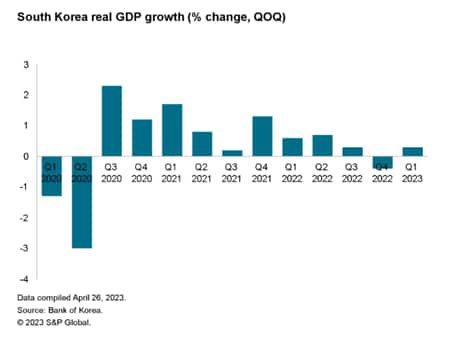

South Korea’s economy surged 2.1% in the first quarter of 2026, exceeding forecasts and marking its fastest growth since mid-2020, driven by a 14.2% jump in semiconductor exports as global demand for AI chips rebounded, according to preliminary data from the Bank of Korea released on April 23, 2026. This performance not only underscores Seoul’s pivotal role in the global tech supply chain but also signals a broader revival in Asian manufacturing that could ease inflationary pressures worldwide and influence monetary policy decisions from Washington to Frankfurt.

Here is why that matters: when South Korea’s chip factories run hot, the ripple effects touch everything from smartphone assembly lines in Vietnam to data centers in Ireland. The country accounts for nearly 17% of global semiconductor production and over 30% of memory chips, making its Q1 surge a leading indicator for tech-dependent economies. After two years of inventory correction and weak consumer electronics demand, the rebound suggests the global tech downturn may be bottoming out—a development closely watched by central banks still grappling with whether to cut interest rates amid persistent services inflation.

The nut graf is this: South Korea’s Q1 strength isn’t just about chips—it’s a barometer for the health of the global AI supply chain and a test of resilience in U.S.-aligned tech alliances. As Washington pushes for “friend-shoring” through initiatives like the CHIPS Act and the Semiconductor Supply Chain Security Pact with Japan and Taiwan, Seoul’s performance validates the strategy of diversifying chip production while maintaining deep integration with trusted partners. Yet this growth also intensifies strategic competition with China, which is accelerating its own semiconductor self-sufficiency drive amid export controls on advanced equipment.

Late Tuesday, as the Bank of Korea’s data flashed across trading floors, analysts at the Korea Institute for International Economic Policy (KIEP) noted that the export surge was broad-based, with automobiles and petrochemicals also contributing to growth. “This isn’t a one-sector story,” said Dr. Ji-young Lee, senior research fellow at KIEP, in a briefing with foreign diplomats in Seoul. “The chip boom is lifting domestic investment and consumer confidence, which means Korea’s recovery has legs beyond external demand.”

But there is a catch: the same global demand fueling Seoul’s growth is tightening competition for advanced chipmaking equipment, particularly extreme ultraviolet (EUV) lithography machines from ASML of the Netherlands. With lead times now stretching beyond 18 months and U.S. Export restrictions limiting sales to China, South Korean firms like Samsung and SK Hynix are locked in a quiet race with Taiwan’s TSMC for priority access. In Washington, officials acknowledge the tension. “We wish resilient supply chains, but we also don’t want to incentivize over-concentration in any single allied nation,” said a senior U.S. Commerce Department official on condition of anonymity, adding that the administration is reviewing incentives to encourage more balanced regional investment under the CHIPS Act framework.

The geopolitical subtext is impossible to ignore. South Korea’s export-driven model has long made it a bellwether for global trade health, and its Q1 performance comes at a moment of heightened strategic realignment. Earlier this month, President Yoon Suk-yeol hosted a trilateral summit with Japan and the Philippines to strengthen maritime security cooperation—a move seen as countering China’s assertiveness in the South China Sea. Economically, Seoul is deepening ties with India through a proposed upgrade to the Comprehensive Economic Partnership Agreement (CEPA), aiming to reduce reliance on Chinese manufacturing while tapping into India’s growing digital economy.

To contextualize the shift, consider the following comparison of semiconductor export reliance among key Asian economies in 2025:

| Economy | Semiconductor Exports (% of Total Exports) | Top Destination for Chip Exports |

|---|---|---|

| South Korea | 38.2% | China (including Hong Kong) |

| Taiwan | 42.7% | China (including Hong Kong) |

| Japan | 18.5% | United States |

| Singapore | 22.1% | China (including Hong Kong) |

Despite political friction, economic interdependence remains stark: over 40% of South Korea’s semiconductor exports still flow to China, including Hong Kong—a figure that creates both leverage and vulnerability. This duality shapes Seoul’s foreign policy, which seeks to maintain robust trade with Beijing while aligning more closely with Washington on technology security. As Dr. Min-joo Park, former deputy minister of trade and now a fellow at the Asan Institute for Policy Studies, observed in a recent panel: “Korea’s challenge is not choosing between China and the U.S., but managing the cost of straddling both. Our growth depends on global openness, not blocs.”

The deep dive reveals a broader pattern: South Korea’s Q1 rebound mirrors similar upticks in export-oriented economies like Vietnam and Mexico, suggesting a synchronized restocking phase in global supply chains. According to the World Trade Organization’s April early estimate, merchandise trade volume grew 1.8% quarter-on-quarter in Q1 2026—the first positive reading since Q3 2023—largely driven by electronics and machinery. This synchrony reduces the risk of isolated overheating and supports the case for a soft landing in global inflation, a scenario increasingly priced into bond markets from New York to Sydney.

Still, risks linger. The won’s 3.1% appreciation against the dollar since January has begun to squeeze exporters’ margins, prompting the Bank of Korea to signal caution about further tightening. Meanwhile, domestic household debt remains elevated at 102% of GDP, limiting the stimulus potential of consumer spending. And while chip prices are recovering, they remain volatile—DRAM contract prices are up 22% quarter-on-quarter but still 35% below their 2022 peak, according to TrendForce.

Looking ahead, the takeaway is clear: South Korea’s Q1 performance is more than a national economic win—it’s a data point in the recalibration of global tech power. For investors, it reinforces the case for strategic exposure to Asian tech supply chains. For policymakers, it highlights the need to balance alliance-building with economic realism. And for the rest of us, it’s a reminder that in an interconnected world, the fate of a memory chip factory in Giheung can shape the pace of innovation—and inflation—half a world away.

What does this imply for the next phase of the global tech cycle? That’s the question worth watching as we head into the second quarter.