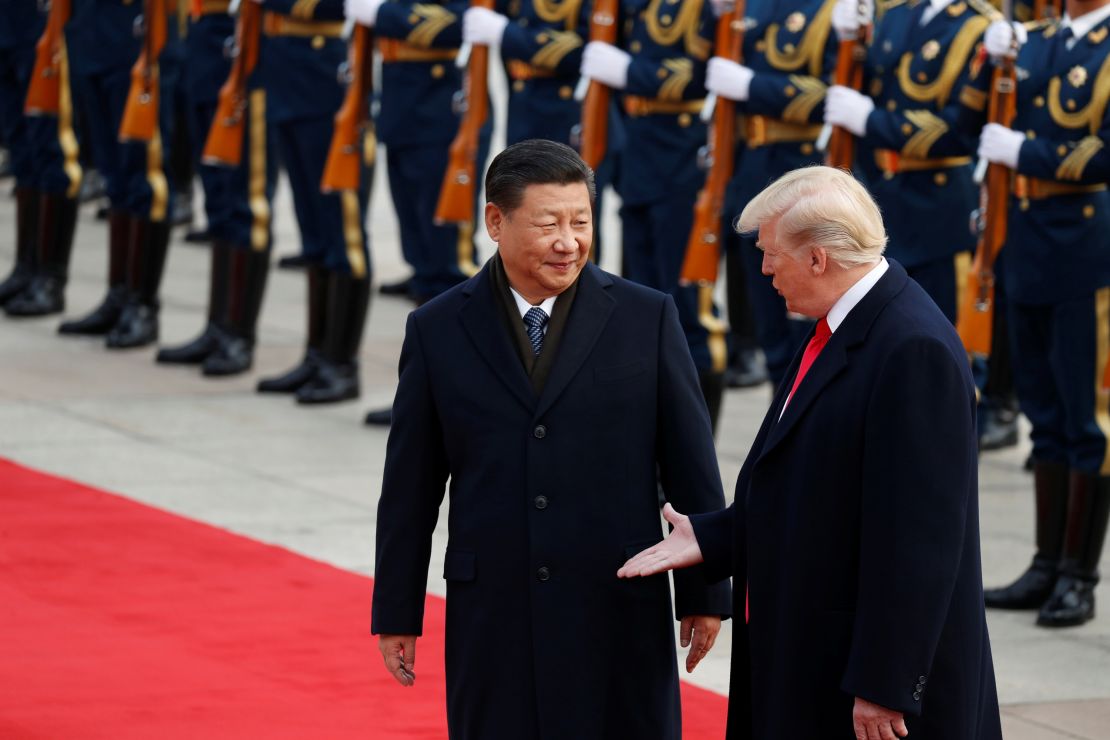

As U.S. President Donald Trump prepares to arrive in Beijing in mid-May for a high-stakes summit with President Xi Jinping, China is positioning itself not merely as a host but as a strategic architect of a recalibrated global order—leveraging economic statecraft, diplomatic outreach, and technological assertiveness to shape the terms of engagement long before the handshake occurs. This coming weekend, senior Chinese officials concluded a series of backchannel engagements with European and Asian counterparts, signaling Beijing’s intent to frame the Trump-Xi meeting as a pivot point for managing systemic rivalry rather than escalating it.

Here is why that matters: the outcome of this summit will reverberate far beyond the bilateral relationship, influencing global supply chain realignments, the trajectory of emerging technology governance, and the credibility of multilateral institutions already strained by geopolitical fragmentation. With the U.S. And China collectively accounting for over 40% of global GDP, their ability to manage competition without decoupling remains a linchpin of international stability.

Earlier this week, China’s State Council released its 2026 Foreign Economic Relations White Paper, detailing a renewed emphasis on “constructive coexistence” with major powers while accelerating self-reliance in semiconductors, green energy, and advanced manufacturing. The document, reviewed by Xinhua and cross-referenced with Ministry of Commerce data, notes that China’s foreign direct investment (FDI) outflows rose 8.3% year-on-year in Q1 2026, with Southeast Asia and Africa absorbing 61% of the increase—a clear signal of strategic diversification away from over-reliance on Western markets.

But there is a catch: while Beijing seeks to project stability, its actions in the South China Sea and support for Russia’s wartime economy continue to raise alarms in Washington, and Brussels. Satellite imagery analyzed by the Center for Strategic and International Studies (CSIS) shows a 30% increase in naval militia activity near Second Thomas Shoal since February, complicating any narrative of de-escalation.

China’s Economic Statecraft: Beyond the Summit Table

Long before Air Force One touches down at Beijing Capital International, Chinese policymakers have been quietly reshaping the economic terrain. The People’s Bank of China (PBOC) maintained the one-year loan prime rate at 3.1% in April, a deliberate signal of monetary stability amid global rate volatility. Meanwhile, the Ministry of Commerce reported that exports to ASEAN grew 12.7% in Q1 2026, outpacing shipments to the U.S. And EU combined—a trend underscoring the success of China’s “dual circulation” strategy, which prioritizes domestic demand while deepening ties with Global South partners.

This shift is not merely tactical. It reflects a broader recalibration of global value chains. According to UNCTAD’s 2026 World Investment Report, China’s share of global electronics manufacturing dipped to 28% from 32% in 2023, yet its share of high-value-added assembly and testing rose to 41%, indicating a move up the value chain. Simultaneously, Vietnam and Mexico have captured much of the labor-intensive export shift—a dynamic Beijing now seeks to influence through infrastructure financing and industrial cooperation.

“China is not retreating from globalization; We see reengineering it on terms that reduce vulnerability to external pressure while maintaining deep integration where it serves its interests,”

— Dr. Linda Yueh, Fellow at St Edmund Hall, Oxford University, and former Chief Economist at the European Bank for Reconstruction and Development, in an interview with the Financial Times, April 10, 2026.

This nuanced approach extends to currency policy. The renminbi’s share in global trade settlements reached 4.8% in March 2026, up from 3.2% in 2022, according to SWIFT data—a gradual but deliberate effort to reduce dollar dependency without triggering capital flight. The PBOC’s cross-border interbank payment system (CIPS) now processes over 1.3 million transactions monthly, a 44% increase from two years ago, though still dwarfed by SWIFT’s volume.

The Security Shadow: Where Diplomacy Meets Deterrence

While economic engagement dominates the headlines, China’s military modernization continues apace, casting a long shadow over the summit’s tone. The 2026 Defense White Paper, released in March, confirmed a defense budget of ¥1.67 trillion (~$230 billion), representing a 6.8% increase—the lowest annual growth rate since 2010 but still the largest in absolute terms globally after the U.S.

More telling than the numbers is the composition of that spending. The International Institute for Strategic Studies (IISS) notes that investment in naval surface combatants and amphibious warfare systems has slowed, while funding for cyber, space, and electronic warfare has risen to 22% of the total defense budget—up from 15% in 2020. This shift suggests a strategic pivot toward asymmetric dominance rather than conventional fleet expansion.

Yet, Beijing’s actions in the East and South China Seas remain a flashpoint. In late March, the Chinese Coast Guard conducted a unprecedented joint patrol with Indonesia’s maritime authority near the Natuna Islands—a move welcomed by Jakarta but viewed with suspicion in Manila and Hanoi, where overlapping claims persist. The patrol, confirmed by both nations’ maritime agencies, underscores China’s effort to cultivate selective partnerships while asserting jurisdictional control.

“The real test of the Trump-Xi summit won’t be what’s said in the Great Hall of the People, but whether both sides can agree on rules of engagement for unavoidable friction points—like Taiwan Strait transits or South China Sea encounters—without letting them spiral,”

— Ely Ratner, former U.S. Assistant Secretary of Defense for Indo-Pacific Security Affairs, now Senior Fellow at the Carnegie Endowment for International Peace, speaking at the Shangri-La Dialogue pre-brief, April 5, 2026.

Global Ripple Effects: Supply Chains, Markets, and the Risk of Miscalculation

The stakes extend well into the global macroeconomy. A sudden deterioration in U.S.-China relations could trigger renewed tariff escalations, disrupting just-in-time manufacturing networks that rely on Chinese components for everything from electric vehicle batteries to pharmaceutical intermediates. The Peterson Institute for International Economics estimates that a 20% increase in tariffs on $300 billion of Chinese goods could raise U.S. Consumer prices by 0.9% and shave 0.3% off global GDP growth—figures that assume no retaliatory countermeasures.

Conversely, a stable, predictable outcome could bolster investor confidence in multinational corporations with deep China exposure. Apple, Tesla, and Siemens all cited China as critical to their 2025 annual reports, with combined revenue exposure exceeding $150 billion. Any perception of increased operational risk—whether from regulatory uncertainty or geopolitical tension—could trigger capital reallocation toward India, Mexico, or Poland, reshaping global industrial footprints over the next decade.

There is likewise a growing consensus among central bankers that the U.S.-China relationship is now a systemic risk factor comparable to climate change or pandemics. In April, the Bank for International Settlements (BIS) included “great power rivalry” in its quarterly review as a structural modifier of financial stability, noting that cross-border lending between U.S. And Chinese banks has declined 18% since 2022, while lending via third-country hubs like Singapore and Luxembourg has risen—a clear sign of financial fragmentation.

A Deliberate Calm Before the Storm?

As the summit approaches, China’s public messaging emphasizes partnership and predictability. State media has highlighted Xi’s recent calls with European Commission President Ursula von der Leyen and Indian Prime Minister Narendra Modi, framing them as evidence of Beijing’s commitment to multipolar dialogue. Yet, behind the scenes, the Communist Party’s Central Committee is reportedly conducting war-game simulations focused on scenarios involving U.S. Arms sales to Taiwan or a sudden closure of Chinese access to advanced chipmaking equipment.

This duality—public conciliation paired with private preparation—is not unique to China, but it defines the current phase of great power relations. The Trump-Xi summit is less likely to produce a grand bargain than a managed reset: an agreement to reopen high-level military-to-military talks, renew cooperation on climate finance, and establish a joint working group on fentanyl precursor regulation—issues where mutual interest exists despite broader estrangement.

The real test will come afterward. Can both sides sustain restraint when domestic pressures mount? Will U.S. Lawmakers resist the temptation to link China policy to electoral cycles? And can Beijing convince its own hardliners that engagement, not confrontation, best serves its long-term interests?

For now, the world watches not just for what is said between two leaders in Beijing, but for what it signals about whether the 21st century’s defining rivalry can be steered away from catastrophe—and toward a fragile, functional coexistence.