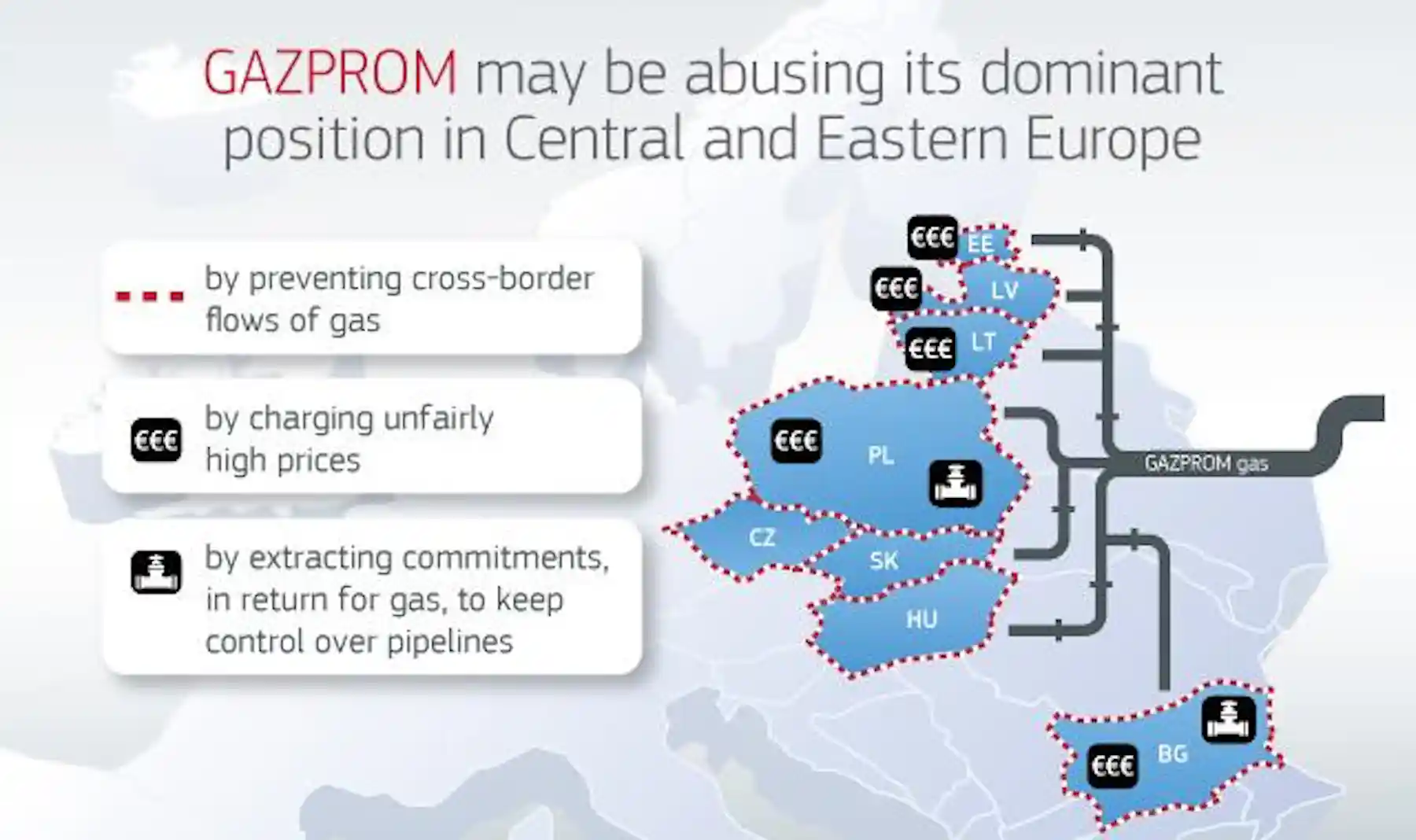

Gazprom (MCX: GAZP), Russia’s state-owned energy giant, has faced a systemic collapse in its European market share and revenue following the 2022 geopolitical pivot. This decline is driven by the weaponization of gas supplies, the loss of high-margin pipeline exports to the EU, and a failure to pivot rapidly to Asian markets.

The erosion of Gazprom is not merely a corporate failure; it is a macroeconomic bellwether. For decades, the European industrial complex relied on cheap Russian feedstock to maintain a competitive edge in manufacturing. As that bridge collapsed, the resulting energy price volatility forced a structural shift in global trade, accelerating the transition to LNG and renewables while permanently altering the balance of power between the Kremlin and the European Commission.

The Bottom Line

- Revenue Hemorrhage: The loss of the European market has created a permanent structural deficit in Gazprom’s cash flow that cannot be offset by Chinese pipeline capacity in the short-to-medium term.

- Capex Paralysis: High sanctions pressure and the exodus of Western technology partners (like Siemens Energy) have stalled critical infrastructure upgrades.

- Macro Shift: The transition from pipeline-dependency to a fragmented LNG-based market has increased costs for European heavy industry, permanently lowering the GDP ceiling for several EU nations.

The Mathematical Reality of the Pipeline Pivot

Here is the math. For years, Gazprom operated on a high-margin, low-overhead model, leveraging existing pipeline infrastructure to dominate the EU. When the flow stopped, the company didn’t just lose customers; it lost its primary source of hard currency.

While the Kremlin points to the “Power of Siberia” pipelines as a solution, the logistics are punishing. Pipeline gas to China is sold at a significant discount compared to historical European contracts, and the volume cannot match the scale of the lost EU market. But the balance sheet tells a different story: the cost of building fresh infrastructure in the East is astronomical, while the revenue per cubic meter is shrinking.

| Metric (Estimated) | Pre-2022 Baseline | 2025/2026 Projection | Variance |

|---|---|---|---|

| EU Market Share | ~40% | <10% | -75% |

| Annual Revenue (USD) | $100B+ | $45B – $60B | -40% to -55% |

| Net Income | Positive/Strong | Net Loss/State-Subsidized | Negative |

Infrastructure Decay and the Technology Gap

The crisis is compounded by a critical lack of technical expertise. Gazprom relies heavily on Western turbines and software for its extraction and transport networks. With the departure of firms like Siemens Energy, the operational risk has increased.

This is where the “Information Gap” becomes apparent. Most analysts focus on the geopolitics, but the real story is the degradation of the physical assets. Without specialized parts, the efficiency of gas extraction in the Yamal peninsula is declining. This creates a vicious cycle: lower efficiency leads to lower output, which leads to lower revenue, which prevents the investment needed to fix the efficiency.

“The Russian energy sector is facing a systemic transition that is less about politics and more about the brutal reality of capital expenditure. You cannot replace 30 years of integrated European infrastructure with a few pipes to Asia without a massive, sustainable capital injection that currently doesn’t exist.”

Market-Bridging: The Winners of the Vacuum

As Gazprom recedes, the vacuum has been filled by a mix of US-based LNG exporters and Middle Eastern suppliers. This shift has directly benefited companies like Cheniere Energy (NYSE: LNG), which has seen its order books swell as European utilities scramble for long-term security of supply.

the volatility has accelerated the adoption of energy-efficient technologies across the Eurozone. The “energy shock” acted as a catalyst for the European Green Deal, shifting capital from fossil fuel imports to domestic renewable infrastructure. This is a permanent reallocation of capital that Gazprom can never reclaim.

But there is a hidden cost. The “energy premium” now paid by European manufacturers—specifically in Germany’s chemical sector—has led to a decline in industrial competitiveness. This is why we see a trend of “de-industrialization” in the heart of Europe, as firms move production to the US or Asia where energy costs are more predictable.

The Geopolitical Trap and Future Trajectory

Gazprom is no longer a commercial entity; it is a state utility tasked with funding a war effort. When a company’s primary objective shifts from profit maximization to geopolitical leverage, the market value inevitably collapses. The Reuters and Bloomberg terminals reflect this through the extreme volatility and lack of liquidity in Russian assets.

Looking ahead to the close of the current fiscal cycle, expect Gazprom to rely further on state bailouts to cover operational losses. The company’s forward guidance is essentially nonexistent because its destiny is tied to the Kremlin’s diplomatic whims rather than market demand.

The trajectory is clear: Gazprom is transitioning from a global energy hegemon to a regional supplier with a decaying asset base. For the global investor, the lesson is simple: infrastructure is only as valuable as the political stability of the contracts that support it.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.